One of the biggest challenges faced by our growing economy in coming days is providing affordable housing, sanitation and a safe environment to the Citizens. Real estate prices have also skyrocketed over the past couple of decades leaving the common man with only dreams of owning a house. As per KPMG report the housing need is almost equally distributed in urban and rural areas in the range of 5 to 6 crore units.

The analysis of KPMG is given below:

Prime Minister envisioned Housing for All (HFA) by 2022 when the Nation completes 75 years of its Independence. In order to achieve this objective, Central Government has launched a comprehensive mission “Housing for All by 2022- Pradhan Mantri Awas Yojana.

Prime Minister envisioned Housing for All (HFA) by 2022 when the Nation completes 75 years of its Independence. In order to achieve this objective, Central Government has launched a comprehensive mission “Housing for All by 2022- Pradhan Mantri Awas Yojana.

However, making housing affordable is not an easy task. Around 20-30% goes in form of various taxes and fees such as Stamp duty, registration fees, service tax, Value added tax. Further, Real Estate Developers have to pay income tax of 30% for profit earned from constructions business.

100% deduction for profit & gain derived from Construction business :

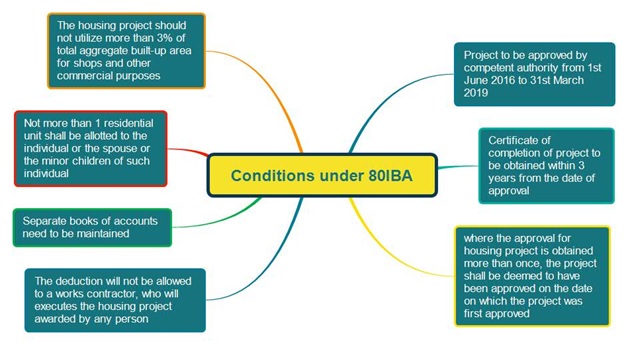

To make purchase of house affordable and give tax incentives to Real Estate Developers Government in the current Union Budget 2016, have announced 100% deduction of the profits and gains derived from construction business, by insertion of new section 80 IBA of Income Tax Act, 1961. Following are the conditions under the scheme:

Certain other conditions has been prescribed with respect to project size and residential unit as enumerated below:

| Sl. No | Metro* | Non- Metro |

| Minimum size of Project | Plot size of land should not be less than 1000 sq. mtrs. | Plot size of land should not be less than 2000 sq. mtrs. |

| Residential unit Size | Does not exceed 30 sq. mtrs. | Does not exceed 60 sq. mtrs. |

| Project Utilization of Floor area ratio | Not less than 90% permissible under rules made by Government or local authority | Not less than 80% permissible under rules made by Government or local authority |

Metro: Chennai, Delhi, Kolkata or Mumbai or within the area of twenty-five kilometers from the municipal limit of these cities.

Illustration: Bangalore is a non-metro city. Hence, plot size of land should not be less than 2000 sq. mtrs. Maximum residential size should not exceed 60 sq. mtrs.

Impact of non-compliance: In case where the housing project is not completed within the period specified, the total amount of deduction so claimed and allowed in one or more previous years, shall be chargeable to Tax under the head “Profits and Gains of Business or Profession” for the previous year in which for completion so expires.

Author Note: The Focus on Real estate has been kept intact, by giving various tax incentives to Real Estate Builder in the forms of exemption from service tax & Income tax to make housing sector affordable. Deduction limit has also been raised by 50,000/- for first time home buyers within overall limit ceiling limit on loan & price of property.

No comments:

Post a Comment